Any kind of project is embedded in an environment of stakeholders, funds, risks, quality criteria, procurement processes, politics, ethnics and numerous others, that more or less affect progress and success.

How to monitor these and keep control without setting confusion?

Two project indicators usually bundle the influencers and are consequently the dominating indicators – Time and Cost and the Earned Value Analysis is the perfect tool to bring those together.

The way to do it is common project management knowledge:

- Generate a Work Breakdown Structure (WBS) as detailed as deemed adequate

- Prepare a budget based on proper cost estimates for each package in your WBS

- Prepare a time schedule based on your WBS

Now bring that all into context and you know how much a work package will cost and how long will it take when to implement.

In other words, you have generated the Planned Value (PV) of the work packages in the context of your time line. Adding them up and plotting cost over time derives a cumulated S-curve providing the baseline of your monitoring tasks.

Earned Value (EV), as a quantity, represents the amount of work achieved at any given time. There are numerous ways to determine the EV such as measuring as much as reasonable the percentage of completion of the tasks or work packages and multiply with the PV or you could make an assessment of the value of the works complete according to your spec book.

The next indicator you need is the one that represents the costs incurred so far or the Actual Costs (AC). If you have prepared and recorded these three indicators as good and detailed as deemed adequate, you have what you need for controlling your project using the Earned Value Approach.

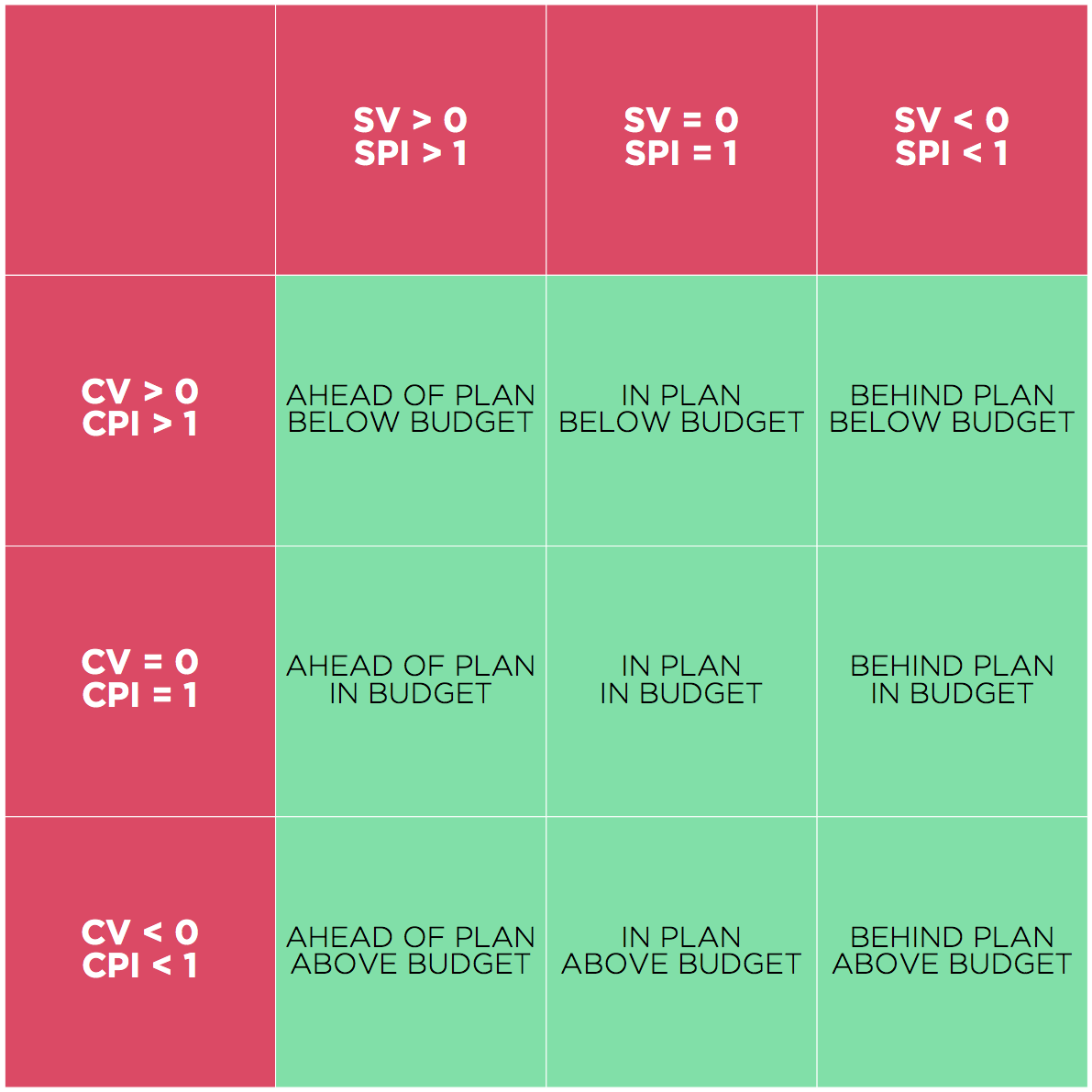

A set of easy to calculate indicators will help monitoring progress:

- Schedule Performance Index (SPI). SPI is the ratio of EV divided by PV at given time, i.e. how much of the planed value have you achieved?

- Cost Performance Index (CPI). CPI is the ratio of EV divided by AC at given time, i.e. what did it cost you to achieve this value?

- Schedule Variance (SV). SV is the difference of EV minus PV, i.e. how far behind or ahead the plan are you?

- Cost Variance (CV). CV is the difference of EV minus AC, i.e. how much over or under your planned cost are you?

The following table with SPI, CPI, SV and CV provides a perfect at-a-glance indication about the status of your project.

Practice examples

Example 1

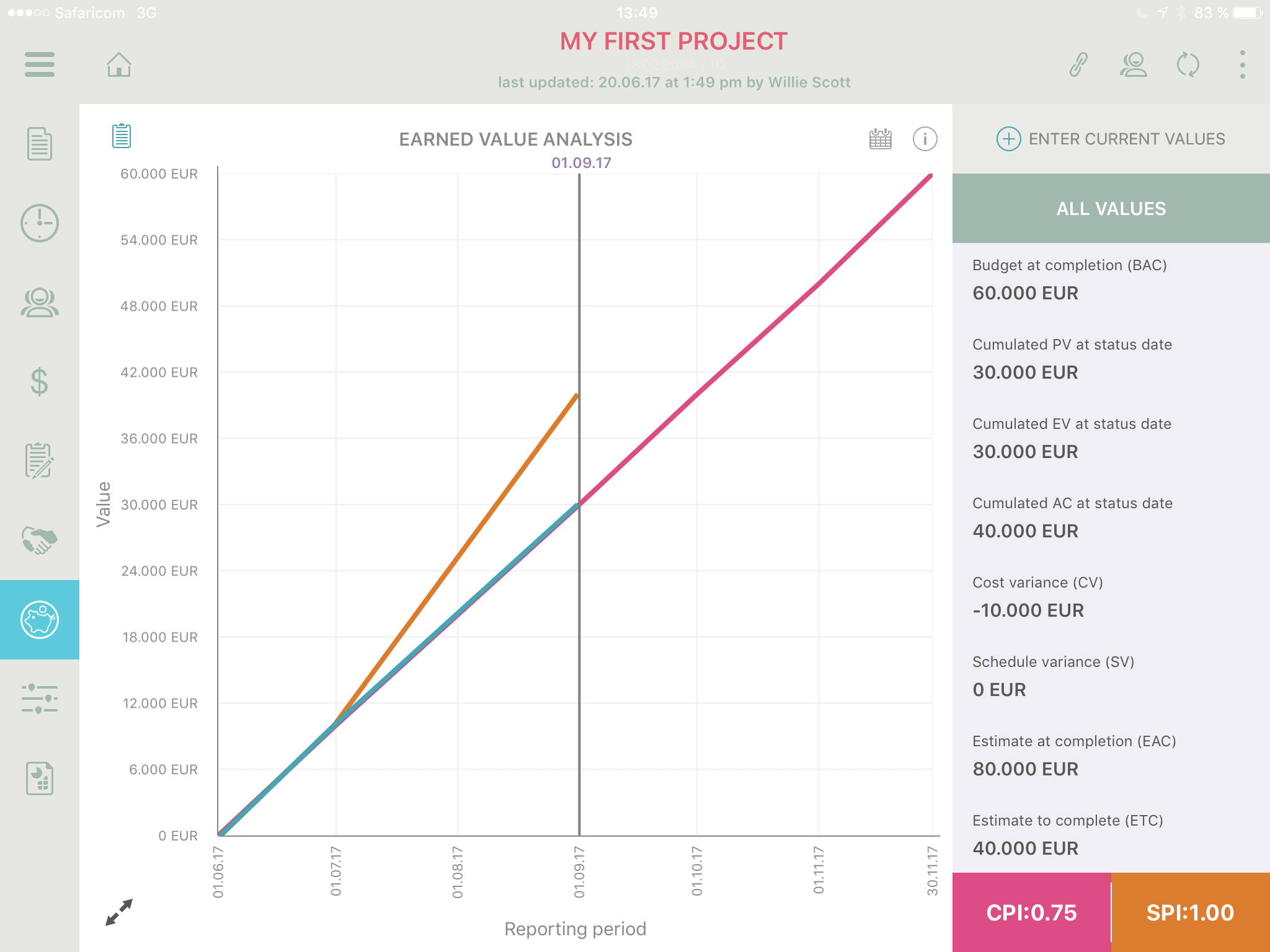

Assume you are running a consulting project over 6 months with a staff contingent you agreed to charge out to your client for a set rate of 10,000 USD per month for working on a certain deliverable.

This would result in a Planned Value (PV) of 10,000 per month or of 60,000 at the end of the project. This is also called Budget at Completion (BAC)

After 3 month you have invoiced your client 30,000 as per your agreement for the monthly payments, which can be interpreted as your Earned Value (EV).

However you have noticed after 1 month that your staffing was not adequately estimated and you were forced to bring in additional experts, which brings your staffing cost to 15,000 per months as of month 2. Subsequently, your Actual Cost (AC) add up to 40,000 after month 3.

Using the Earned Value Approach, you can see that you are on track (EV = PV) but at a higher cost as estimated resulting in a cost performance of only 75%.

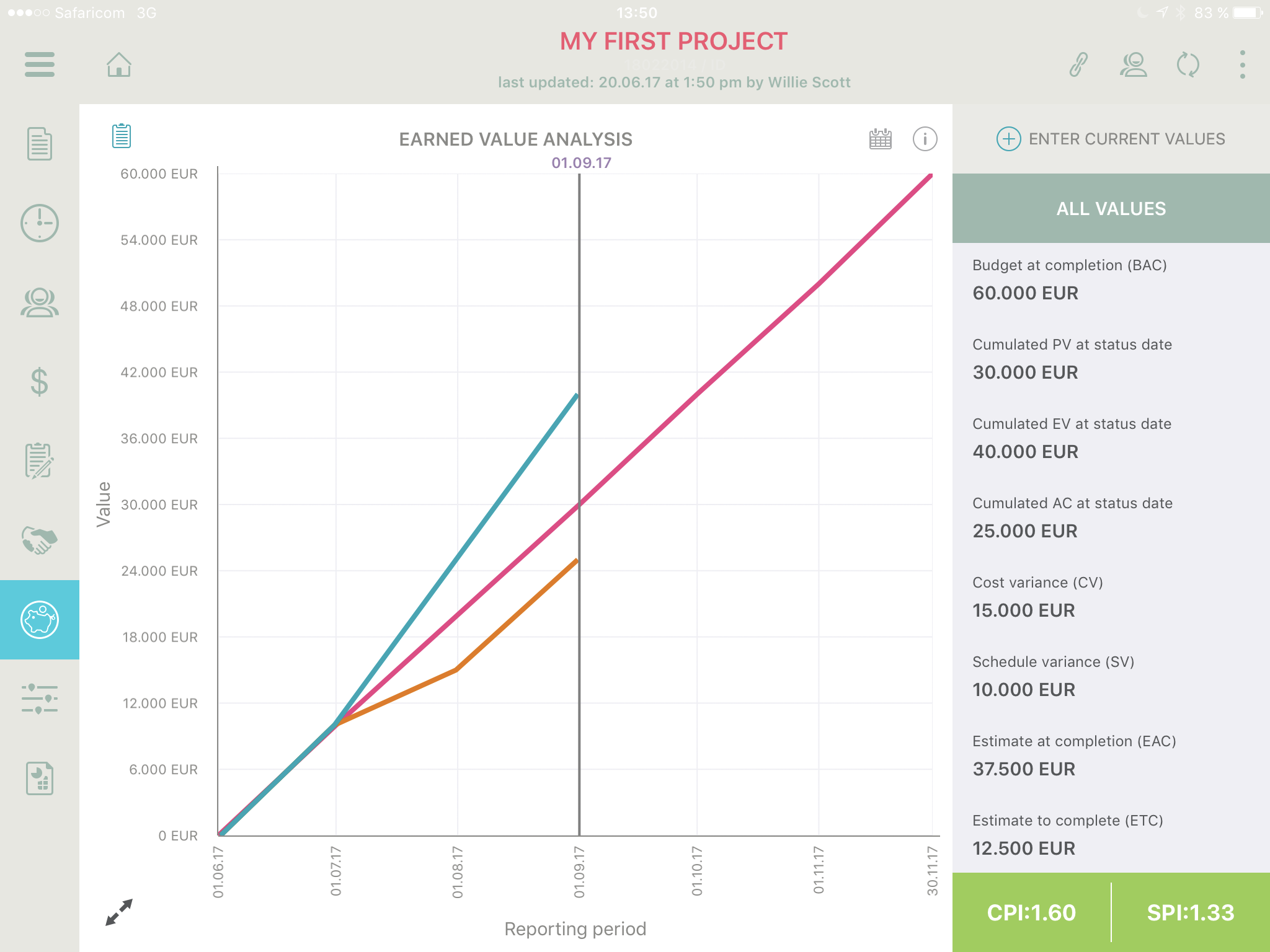

Example 2

In a slightly modified example, your client pays you based on achieved deliverables and not a set rate per month for your staff. Assume that after 3 months you have already created value of 40,000, so you are 10,000 ahead of your plan. Now assume you had actual cost of 25,000 to create this value. Now the Earned Value Analysis shows that you are ahead of time with a schedule performance of 133% and significantly under budget with a cost performance of 160%.

Example 3

This example shows the application of the Earned Value Approach based on project performance in delivering and installing a certain device.

Input data – contract basis

- Contract value (fixed-cost): 9,750,000

- Deliverables: Installation of 150 devices

- Unit rate: 65,000 per device

- Time schedule: 6 months or 25 devices per month

Project control at month 2

PV (planned value) = progress to achieve as planned

- 2 months * 25 devices per month = 50 devices

- 50 * 65,000/device = 3,250,000

EV (earned value) = progress that is achieved

- 40 devices * 65,000/device = 2,600,000

Discrepancy to plan

- 650,000 which is equal to 10 devices

- 10 devices / 50 devices for 2 month = 0.2 months behind plan

You can see that you are behind schedule and your performance is only 80% of what you have planned.

However, you manage to deliver the devices for 55,000 instead of 65,000, which is less than you have budgeted and therefore you have a positive cost performance of 1.18 or 18% better than anticipated.

For the purpose of this example, let’s assume that you had included your profits and overheads in the rate of 65,000 per unit and if EV would equal AC (EV=AC), you would achieve the calculated profits. Since you cost performance is now better by almost 20%, you are running a very healthy project.

#startcollaborating #stopfailing